Understanding Life Insurance Options in 2025: A Complete Guide

Published: April 3, 2025

Life insurance remains one of the most important financial tools for protecting your family's future. As we navigate 2025, the life insurance landscape continues to evolve with new products, features, and purchasing options. At Choice Insurance Agency, we're committed to helping you understand your choices and find the coverage that best meets your needs.

Why Life Insurance Matters in 2025

Despite technological advances and changing financial landscapes, the fundamental purpose of life insurance remains constant: to provide financial security for your loved ones after you're gone. Life insurance can:

- Replace lost income for your family

- Cover final expenses and outstanding debts

- Fund children's education

- Leave a legacy for heirs or charitable causes

- Provide tax advantages and estate planning benefits

- Offer living benefits in certain circumstances

Recent data shows that while 52% of Americans have some form of life insurance in 2025, many remain underinsured, with coverage gaps averaging $200,000 per household.

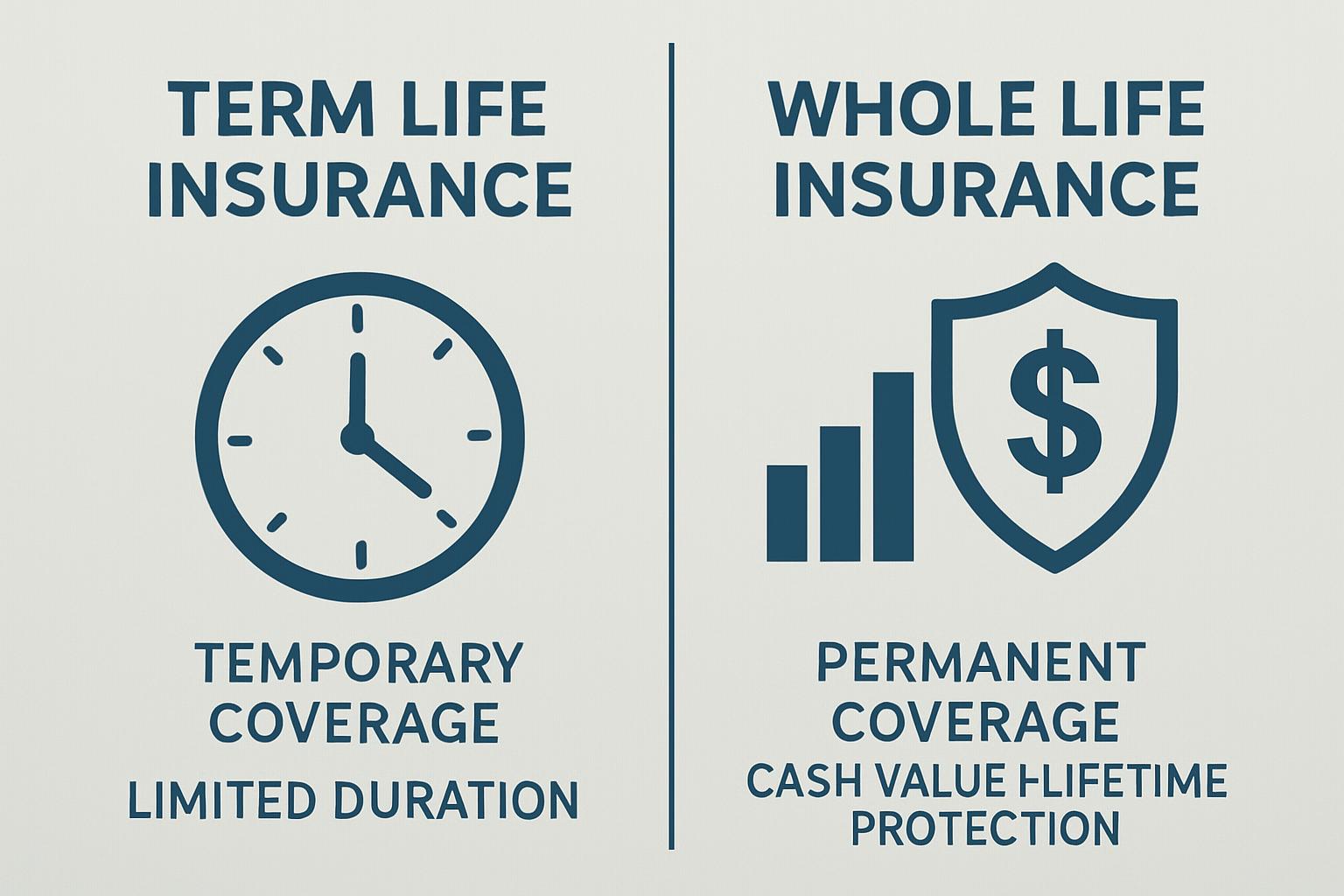

Term vs. Whole Life Insurance: Understanding the Difference

The two primary categories of life insurance continue to be term and permanent (whole life) insurance. Understanding the differences is crucial to making an informed decision.

Term Life Insurance

Key Features:

- Provides coverage for a specific period (typically 10, 20, or 30 years)

- Generally more affordable than permanent insurance

- Offers straightforward death benefits with no cash value component

- Premiums typically increase upon renewal after the term expires

- Some policies offer conversion options to permanent coverage

Term life insurance is often recommended for:

- Young families with children

- Homeowners with mortgages

- Those with specific, time-limited financial obligations

- Individuals seeking maximum coverage at the lowest initial cost

In 2025, a healthy 35-year-old might pay approximately $25-35 monthly for a $500,000, 20-year term life policy.

Whole Life Insurance

Key Features:

- Provides lifetime coverage as long as premiums are paid

- Builds cash value over time that grows tax-deferred

- Premiums generally remain level throughout the policy

- May pay dividends (if from a mutual insurance company)

- Offers various living benefits and loan options

Whole life insurance is often recommended for:

- Those seeking lifetime coverage

- Individuals with long-term dependents (e.g., children with special needs)

- People with estate planning needs

- Those who value the forced savings component

- Business owners for succession planning

For comparison, that same 35-year-old might pay $300-400 monthly for a $500,000 whole life policy in 2025.

Understanding Life Insurance Riders

Life insurance riders are additional benefits that can be added to your policy, often for an additional premium. In 2025, several riders have become increasingly valuable:

Popular Life Insurance Riders in 2025

Accelerated Death Benefit:

- Allows access to a portion of the death benefit if diagnosed with a terminal illness

- Now standard on many policies at no additional cost

- Typically available when life expectancy is 12-24 months

Critical Illness Rider:

- Provides a lump sum payment upon diagnosis of specified critical illnesses

- Common covered conditions include cancer, heart attack, stroke, and organ failure

- Helps cover medical expenses not covered by health insurance

Chronic Illness Rider:

- Allows access to death benefits if unable to perform activities of daily living

- Helps cover long-term care expenses

- Increasingly popular as an alternative to standalone long-term care insurance

How Much Life Insurance Do You Need in 2025?

Determining the right amount of life insurance coverage remains one of the most important decisions. While individual circumstances vary, several approaches can help you calculate your needs:

Common Calculation Methods

Income Replacement Method:

- Multiply your annual income by 10-15 (depending on age and financial obligations)

- Example: $100,000 annual income × 12 = $1,200,000 coverage

DIME Formula:

- Debt and final expenses (mortgage, loans, funeral costs)

- Income replacement (years needed × annual income)

- Mortgage balance

- Education costs for children

Ready to Protect Your Family's Future?

Our life insurance specialists are here to provide personalized guidance and help you find the right coverage for your needs.

Book a Free ConsultationThis blog post is for informational purposes only and is not intended as professional advice. Life insurance products, features, and prices vary by company, location, and individual circumstances. Contact Choice Insurance Agency for personalized guidance.